Some holders of Remote Worker KITAS (E33G) have recently started asking a new question: what happens if the Indonesian tax office sends a letter asking for clarification about tax residency?

This article explains what such a letter usually means, why it may happen, what documents are commonly requested, and what Remote Worker KITAS holders should do next.

The goal of this article is informational only. Flado Visa Agency is not an accounting or tax filing company. We do not provide tax calculations, tax return preparation, tax planning, or accounting services. For tax analysis, tax residency assessment, NPWP registration questions, or income reporting, please contact the Indonesian tax office directly or a licensed tax consultant.

If you are looking for the visa itself, full information about Remote Worker KITAS is here:

https://flado.id/nomad

Why We Are Publishing This

We previously explained that Remote Worker KITAS (E33G) is not a work visa and does not by itself create Indonesian salary taxation. That remains an important and useful starting point.

However, there is now a practical example showing that the tax office may review some long-stay foreigners individually and ask for clarification if a person appears to meet the criteria of an Indonesian domestic tax subject.

This new article does not cancel those explanations. It updates them with a real administrative scenario that some foreigners may face after staying in Indonesia for a long period.

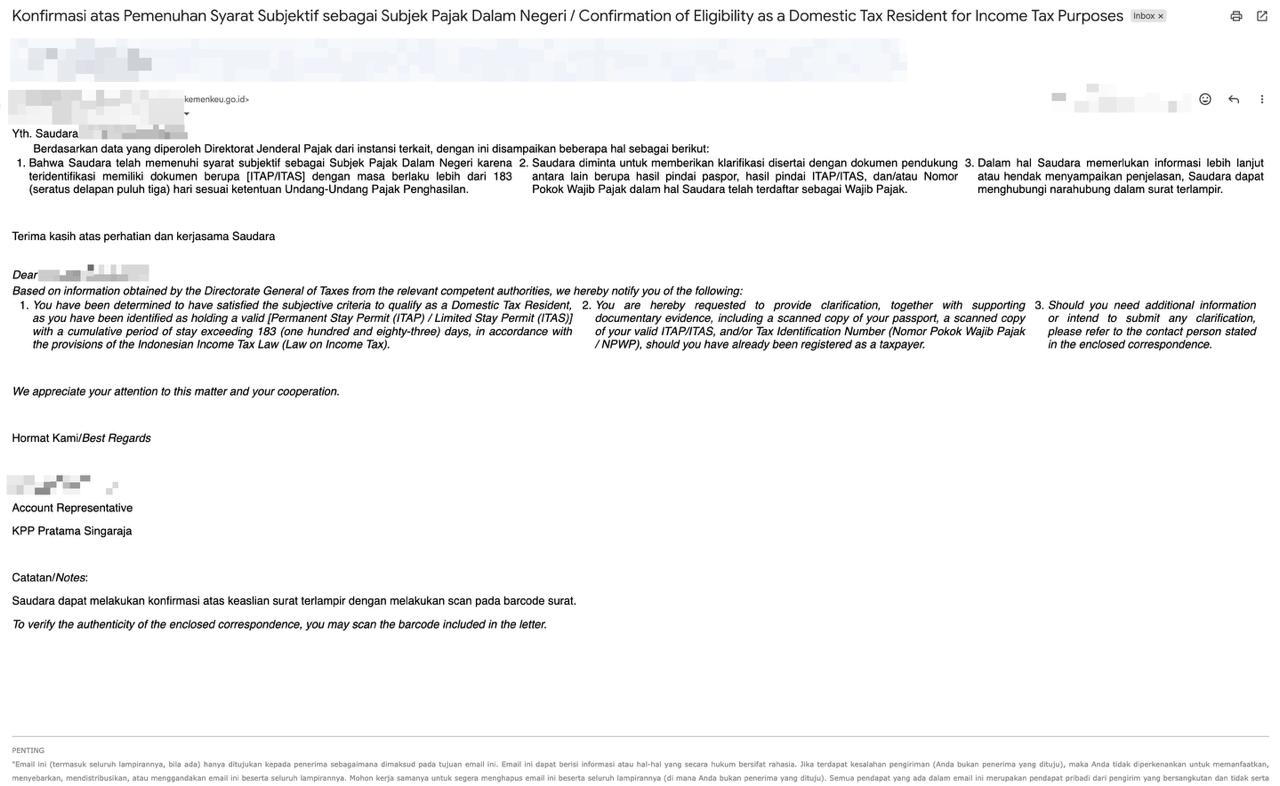

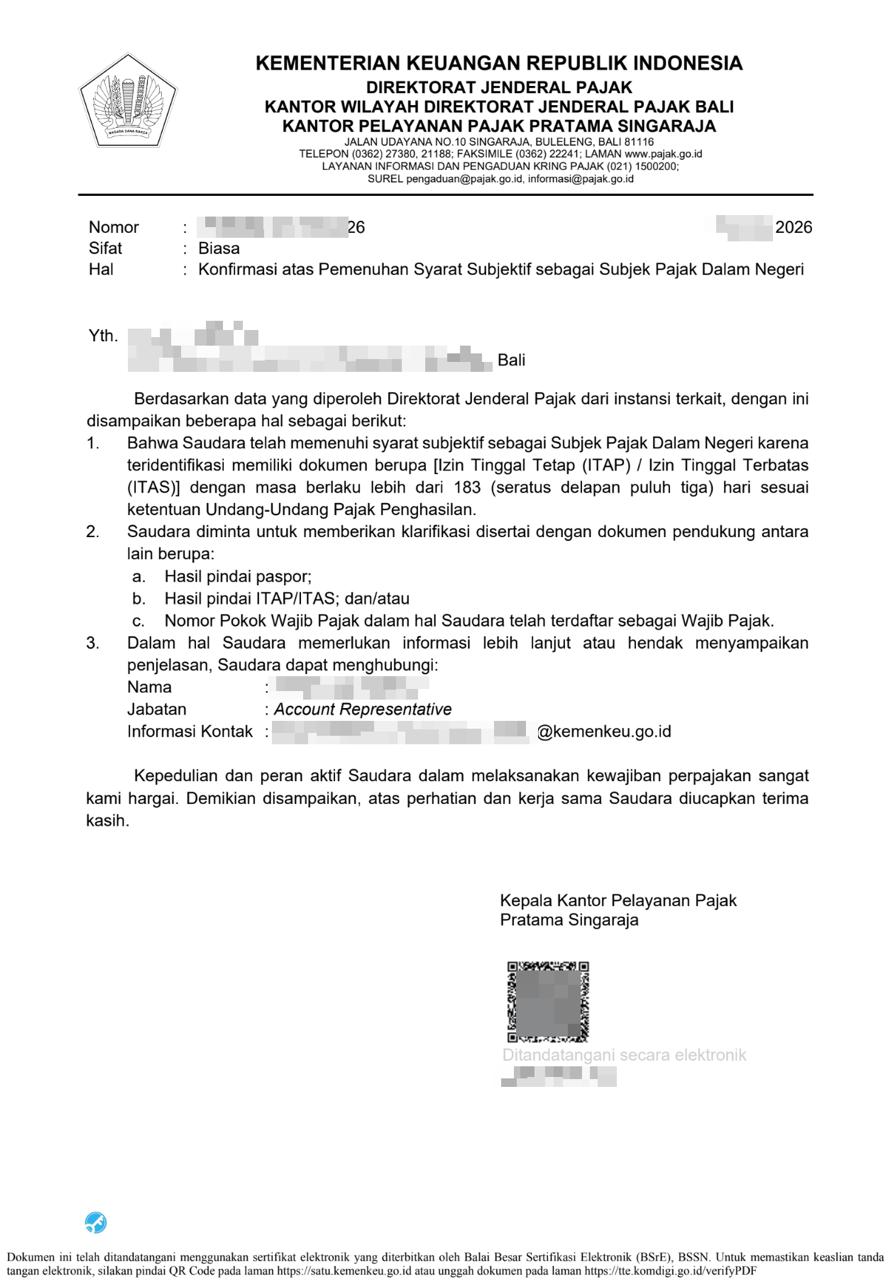

A Real Example of the Letter

Below is a example of the type of letter that may be sent by the tax office.

In this type of letter, the tax office usually states that the person has been identified as meeting the subjective criteria of an Indonesian domestic tax subject and is asked to provide clarification with supporting documents.

Example of the Requested Clarification

The communication may also include or refer to a brief status/request note showing what should be submitted.

Based on the example above, the request may include documents such as:

- a scanned copy of the passport,

- a scanned copy of the ITAS / KITAS or other stay permit,

- NPWP details, if the person has already been registered as a taxpayer in Indonesia.

Does This Mean Remote Worker KITAS Has Become a “Tax Problem”?

No. That would be the wrong conclusion.

Remote Worker KITAS (E33G) is still not a work visa. It is not intended for employment in Indonesia and does not by itself mean that Indonesian salary tax is automatically due.

What this case does show is something more specific: if a foreigner stays in Indonesia long enough, the tax office may review that person’s status separately from the visa category itself.

So the main point is not that E33G suddenly became a bad visa. The main point is that immigration status and tax status are not exactly the same thing.

Why Might Such Letters Be Sent?

On 9 December 2025, the Directorate General of Taxes issued a new regulation on determining who is treated as a domestic tax subject and who is treated as a foreign tax subject in Indonesia.

Official regulation reference:

https://www.pajak.go.id/id/peraturan/penentuan-subjek-pajak-dalam-negeri-dan-subjek-pajak-luar-negeri-0

This matters because long-term stay permit holders may become visible to the tax administration if their stay pattern or residency indicators fall within the criteria used by the tax office.

In practical terms, this means that some holders of residence permits may be reviewed and contacted selectively. It does not mean every Remote Worker KITAS holder will receive a letter, and it does not mean an automatic tax assessment has already been issued.

What Does the Tax Office Usually Mean by “Tax Residency”?

Many foreigners know the common rule about more than 183 days of physical presence within a 12-month period. That remains an important benchmark.

At the same time, Indonesian tax analysis may also look at the broader facts of a person’s stay, including whether the person is considered to be residing in Indonesia or has indications of an intention to stay there.

This is why some foreigners should not rely only on the visa name when thinking about tax questions. The tax office may look at the overall situation, not only at marketing labels such as “remote worker” or “digital nomad”.

If the KITAS Has Already Been Closed, Does the Issue Disappear?

Not necessarily.

If a person previously held a KITAS or ITAS and later left Indonesia, the tax office may still review the past period when that person was present in Indonesia or held a long-term stay permit.

In other words, a closed KITAS may end immigration status, but it does not automatically answer all questions about the person’s earlier tax residency position.

Does Receiving Such a Letter Mean There Is Already a Tax Debt?

Usually, no.

A clarification letter is generally not the same as a tax bill, penalty, or final assessment. In many cases, it is simply a request for documents so the tax office can understand:

- who the person is,

- what stay permit was held,

- whether the person already has an NPWP,

- and whether further tax registration or reporting issues may exist.

That said, such letters should not be ignored. If you receive one, it is better to review the case properly and respond carefully.

What Should a Remote Worker KITAS Holder Check First?

If you receive a tax residency clarification letter, start with these practical questions:

- How many days were actually spent in Indonesia?

- During what exact period was the KITAS / ITAS active?

- Was all income foreign-sourced, or was any income connected to Indonesia?

- Was there any local employer, Indonesian client billing, or local business activity?

- Does the person remain a tax resident of another country, with documents to support that?

These are the kinds of facts that matter more than the visa title alone.

If Your Income Was Fully Foreign-Sourced

For many people using Remote Worker KITAS in the intended way, income remains fully foreign-sourced and there is no local Indonesian employer.

That is still an important distinction. It means the immigration purpose of the visa remains clear. But if the person spent a long time in Indonesia, the tax office may still ask for clarification, registration, or reporting depending on the individual facts.

This is why it is better to think of E33G as an immigration category, while tax residency is a separate analysis.

What If You Start Earning Indonesian-Source Income?

If a foreigner works for an Indonesian company, performs local employment, provides services that generate Indonesian-source income, or otherwise carries out activities treated as local work or local business income, then Remote Worker KITAS is not the correct immigration category for that purpose.

Information on work KITAS categories:

https://flado.id/working

In such cases, both immigration compliance and tax compliance should be reviewed separately and properly.

What Documents May Be Needed

If the tax office asks for clarification, prepare the documents carefully. Depending on the case, these may include:

- passport scan,

- KITAS / ITAS scan,

- NPWP, if already available,

- travel history or entry / exit timeline,

- documents supporting foreign tax residency or foreign income origin, where relevant.

Do not send random explanations without first understanding the facts of the case.

How to Get an NPWP in Indonesia If Needed

If tax registration becomes necessary, a foreigner may apply for an Indonesian tax number (NPWP) through the tax administration system and upload the required documents.

As a practical starting point, prepare:

- passport,

- stay permit document,

- other supporting documents requested by the tax office or tax consultant.

If you need help finding the correct tax office or a professional advisor:

Local tax office lookup (KPP Pratama):

https://www.google.com/maps/search/kpp+pratama/@-8.7456143,115.1890519,13z

Tax consultants in Indonesia:

https://www.google.com/maps/search/tax+consultant/@-8.7456143,115.1890519,13.09z

Annual Tax Reporting

If a person is required to report in Indonesia, this is generally done through an annual tax return (SPT Tahunan).

The reporting obligation, timing, and final tax payable depend on the person’s residency status, income structure, and any applicable treaty or special regime. Because of that, filing should be reviewed individually by the tax office or a qualified tax professional.

Flado Visa Agency does not provide annual tax return filing, tax calculations, or accounting services.

Important Practical Conclusion

Remote Worker KITAS (E33G) remains a valid and useful immigration option for foreigners who want to stay in Indonesia while earning from outside Indonesia.

At the same time, long stays may create a separate tax review issue in some cases. A tax residency clarification letter does not automatically mean wrongdoing, tax debt, or a problem with the visa itself. It means the tax office wants documents and clarification.

The correct approach is simple:

- do not panic,

- do not ignore the letter,

- check your days of stay and income source carefully,

- contact the tax office or a licensed tax consultant if needed.

If you need help with the visa side, our team will be glad to assist with immigration matters. If you need help with tax residency analysis, NPWP, or tax reporting, please contact the tax office directly or a professional tax consultant, as these services are outside the scope of Flado Visa Agency.